What is an OPEB Obligation Bond and Should You Consider One?

Bottom Line Up Front

- OPEB Obligation Bonds (OOBs) are issued by municipalities to prefund their OPEB obligation through an OPEB Trust

- These bonds are used to increase the municipality’s OPEB discount rate and decrease its Total OPEB Liability (TOL), but there are downsides that should be considered first.

- GFOA has issued an advisory regarding OOBs due to the considerable risk involved.

An OPEB Obligation Bond (OOB) is a debt instrument issued by a municipality to prefund their OPEB obligation bond through an OPEB Trust.

The argument is that a municipality can generally borrow money at lower rates than an investor would expect to earn in the capital markets over the long term. Additionally, when you are prefunding your OPEB liability, GASB 75 may allow the use of a higher discount rate, thereby reducing the disclosed OPEB liability.

How Does an OPEB Obligation Bond Work?

Let’s look at an example with some numbers to get a better idea of how this works:

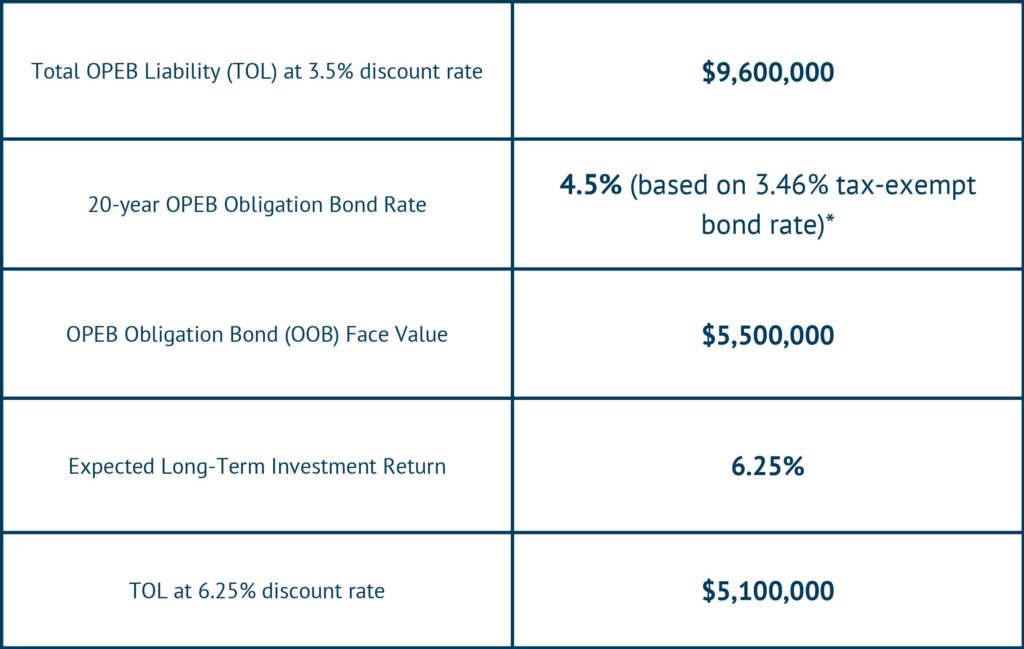

Looking at the figures above, Town of X borrows $5.5 million in the bond market to prefund their OPEB liability. They invest that money in an OPEB Trust which decreases their Total OPEB Liability from $9.6 million to $5.1 million. This happens because we got to increase the discount rate from 3.50% to 6.25% based on their asset level and investment policy.

That’s amazing, right?! With one little “trick” the Town of X decreased its disclosed liability by $4.5 million! They did that while taking advantage of an “arbitrage” opportunity. That $5.5 million in the OPEB Trust expects to earn 6.25% per year while the Town is only paying 4.50% on the Bond. Now, the Town must make interest payments of $247.5k per year in profit.

That’s a great deal! At least, that’s the pitch the OOB salesman will give you.

4 Reasons OPEB Obligation Bonds Are Too Good to Be True

You’re probably sitting there saying, “Kurtis, that sounds amazing. Why isn’t everyone doing this? What’s the catch?

1. Return on investments aren’t guaranteed

First, the nature of an OOB is to convert an annual “pay-as-you-go” cost plus a variable annual OPEB Trust contribution into a fixed cost with coupon payments due. But the return on investment is not guaranteed. A long-term investment expects to earn 6.25%, but year-to-year it could lose money, gain up to 20%, or anything between.

To issue an OOB, you’d have to be ready and willing to make the coupon payments each year. They may or may not be more than our annual “pay-as-you-go” OPEB costs. And you will still need to accumulate enough funds to retire the bond at maturity.

2. You can’t use the funds or returns to pay back the bond

There is also the consideration of paying back the face value of the Bond in 20 years. In theory, the money is available because it has been growing in an investment account. However, once those funds go into an OPEB Trust they can only be used to pay for OPEB benefits.

This would force the Town to manage their OPEB withdrawal and annual funding to establish a sinking fund outside of the OPEB Trust. Those funds are likely not going to be invested as aggressively thus cutting into the total return on the OOB funds and eating into or even eliminating the “arbitrage” profit.

3. OPEB benefits are volatile

Additionally, OPEB benefits are much more volatile than Pension benefits and can easily change by more than 10% over a two-year valuation cycle. Issuing debt to fund the TOL, then finding that because of the volatility, the plan is no longer fully funded (which may also cause the discount rate to decrease which further increases the liability) is a risk that cannot be mitigated.

4. OPEB Obligation Bonds are most popular when the markets are hot

My last concern with OOBs, has to do with timing and investment strategy. OOB’s and their counterpart, Pension Obligation Bonds, have been most popular when financial markets are soaring.

When people are excited and everyone is making money in the financial markets, it often becomes appealing to try and leverage your position to maximize those gains for yourself. This is basic investment psychology.

The problem is that when markets are running hot and high, they tend to be getting towards the end of a market cycle and getting ready for a correction. Because of the basic psychology of investing everyone tends to pile in just in time to see financial markets decline.

This becomes a much bigger problem when your position is leveraged. When is the next market correction coming? I don’t know! I do know that the best time to take advantage of an OOB is when markets are down and interest rates are dropping as the FED tries to stimulate the economy. I also know that is when nobody is talking or even thinking about OOB’s (see March of 2020 when capital markets collapsed amid the COVID crisis).

Should You Consider Using an OPEB Obligation Bond as Part of Your OPEB Funding Strategy?

Yes, absolutely consider it, but make sure that when you do, you’re weighing all the pros and cons. Make sure that your Town is ready to take on a leveraged investment with the ensuing volatility that comes with it. In our experience, most Towns are not ready for this level of volatility.

If you can picture your Town Board or Mayor having a conversation with taxpayers about how the fund is down and we are still making interest payments, but we need to ride it out and we’ll be fine on the other side, then you’re there. If you’d do anything to avoid that conversation, then this isn’t the strategy for you.

A final word of caution, the Government Finance Officers Association (GFOA) has issued an advisory that, “State and local governments should not issue OPEB bonds for a variety of reasons.” Issuing an OOB may work out in some circumstances, but it should be done with an extreme dose of caution.

If you still have questions regarding OPEB Obligation Bonds, you can reach me here.

About The Author Kurtis has been a consultant on the Odyssey Advisors team since 2013 and has developed extensive knowledge and expertise in developing and administering retirement benefit solutions. Kurtis is passionate about helping people achieve the retirement they’ve always dreamed of...

More Insights From This author