Can I have a Solo 401(k) and a Company 401(k)?

Bottom Line Up Front

- If you have a full-time job and a side business with no employees, you can contribute to both a regular 401(k) and a Solo 401(k).

- Employee contributions are capped at $23,500 total across all 401(k) plans in 2025 ($31,000 if 50+).

- Employer contributions are separate for each plan – each employer can contribute up to $70,000, but this amount is reduced by any employee contributions made to that plan.

- If you contribute the full $23,500 as an employee, the maximum combined employer contributions across both plans would be $116,500, bringing the total possible contributions to $140,000 ($147,500 if 50+).

Absolutely! If you have a 9-to-5 with a company 401(k) plan and a side hustle with 1099 income, you might be leaving money on the table if you’re not using a solo 401(k). Many people don’t realize that having multiple income streams means you can also have multiple retirement plans – allowing you to stack contributions and maximize tax savings.

Unlike IRAs, which have a hard cap on contributions no matter how many you have, 401(k) plans work differently. Your side business opens the door to another retirement account, allowing you to save even more. The best part? You get to play both roles: employer and employee, meaning you can potentially sock away thousands more in tax-deferred (or tax-free, if Roth) savings. Let’s break down how it works.

Why Having Two Retirement Plans Can Be a Smart Move

Many people assume that if they have a 401(k) through their employer, they’ve maxed out their retirement contributions—but that’s not entirely true. If you also have a side business with a Solo 401(k), you have additional tax-advantaged savings opportunities. The key is understanding how the limits work.

A 401(k) has two types of contributions:

- Employee Contributions: This is the portion you contribute from your paycheck or side business income. In 2025, the total employee contribution limit is $23,500 across all 401(k) plans ($31,000 if you’re 50+).

- For example, if you contribute $10,000 to your employer’s 401(k), you can only contribute $13,500 more as an employee across either your employer’s plan or your Solo 401(k).

- For example, if you contribute $10,000 to your employer’s 401(k), you can only contribute $13,500 more as an employee across either your employer’s plan or your Solo 401(k).

- Employer Contributions (Profit-Sharing): This is where things get interesting. Employer contributions are separate for each plan because they’re based on each employer’s earnings.

- Employer contributions are separate for each plan, meaning each employer can contribute up to $70,000, but this amount is reduced by any employee contributions made to the plan.

- If you maximize employee contributions ($23,500), the combined employer contributions across both plans would be $116,500.

- Employer contributions are separate for each plan, meaning each employer can contribute up to $70,000, but this amount is reduced by any employee contributions made to the plan.

Unlike employee contributions, where the limit is shared across plans, the employer contribution limit applies separately to each plan – which is why a Solo 401(k) can be a powerful tool for increasing retirement savings.

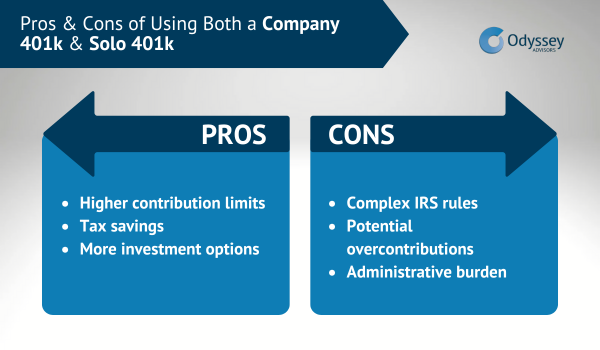

Perks of Having Both a 401(k) and a Solo 401(k)

- Double the Savings Potential: While you’re limited on employee deferrals, employer contributions give you another bucket of tax-deferred savings. You get to wear both hats and can make contributions as both an employee and employer.

- Lower Your Tax Bill: Contributing more means reducing your taxable income from both your day job and side hustle.

- More Investment Choices: Employer-sponsored 401(k)s often have limited options, while solo 401(k)s can offer more flexibility, including real estate and alternative investments.

- Tax Planning Flexibility: You can choose a Roth or traditional for both plans, letting you balance taxable income now vs. tax-free withdrawals later.

Common Solo 401(k) Misconceptions

“If I max out my work 401(k), I can’t contribute to my Solo 401(k) at all.”

Not true. You can still make employer contributions from your self-employment income, even if you hit the employee limit at your day job.

“Solo 401(k)s are for full-time business owners.”

False! Even if your side hustle only brings in a few thousand dollars a year, you can still take advantage of tax-advantaged savings.

“I should just open a SEP IRA instead.”

Maybe, but Solo 401(k)s generally allow higher contributions at lower income levels because they let you contribute both as an employee and an employer. SEP IRAs only allow employer contributions.

Having two retirement plans isn’t just possible, it’s a smart strategy for anyone juggling a 9-to-5 and a side business. Next, let’s break down how to maximize your contributions without running into issues with the IRS.

Maximizing Contributions Without Overstepping IRS Rules

The key to maximizing contributions is understanding how the IRS limits apply across both plans. Here’s how to make the most of your retirement savings without accidentally contributing too much.

- Know the Two Types of 401(k) Contributions

There are two main types of contributions to be aware of:- Employe Deferrals: You can contribute up to $23,500 in 2025 ($31,000 if 50+) across all 401(k) plans combined.

- Employer Contributions: Your employer (including your own business) can contribute up to 25% of your compensation from each job up to a total of $70,000 for each job (reduced by the amount of your employee contributions to that plan excluding the catch-up).

- Max Out Your Employee Deferrals Wisely

Since the employee contribution limit is shared between both plans, you’ll need to decide where to contribute first:- If your W-2 job offers a match, contribute there first to get free money.

- Once you’ve maxed out your match, you can split additional deferrals between both plans or focus on the one with the better investment options and lower fees.

- Use the Employer Contribution Loophole

Even if you max out employee contributions at your W-2 job, your side business can still contribute to your solo 401(k) as an employer. Here’s how:- Sole Proprietorship / Single-Member LLC: Employer contributions are 20% of the net self-employment income (after deducting half of your self-employment tax).

- S-Corp: Employer contributions can be 25% of your W-2 wages from the business (not total revenue). Remember that S-Corp dividends are NOT considered compensation for retirement plan purposes.

- Consider Roth vs. Traditional Contributions

If you expect higher income in retirement, Roth contributions (tax-free withdrawals later) might be better. If you want to lower your taxable income now, traditional (pre-tax) contributions make sense.

You can mix and match: Roth for one plan, traditional for another. - Avoid Common IRS Pitfalls

- Excess Employee Deferrals: You can contribute $23,500 to each plan (traditional, Roth, or combined). The limit is shared across every 401(k).

- Miscalculating Employer Contributions: Employer contributions are separate, but they still can’t exceed 25% of your eligible earnings from each employer.

- Missing the Tax Filing Deadline: Solo 401(k) contributions must be made by your business’s tax return deadline (including any extensions). A great tip? Set a calendar or phone reminder for when you want to contribute.

- Track Contributions and Work with a Tax Pro

401(k) rules can be complicated – especially with multiple plans. Keep a running total of contributions throughout the year and work with an accountant, TPA, or financial advisor to stay within IRS guidelines.

The Bottom Line

By strategically using both a Solo 401(k) and an employer-sponsored 401(k), you can maximize tax-deferred (or tax-free) savings, reduce your taxable income, and accelerate your retirement goals as both an employer and employee. It definitely pays to know your retirement plan options.

Keep in mind that you need to understand the difference between employee and employer contributions to avoid overstepping IRS rules. That’s why it’s important to work with an experienced retirement third-party administrator, financial advisor, or tax pro to ensure you’re making the most of your savings while staying compliant.

About The Author Stephanie joined the Odyssey Advisor’s team all the way from the Lonestar state in November of 2020. She is versatile in her abilities and has experience in copywriting, photography, and analytics. She helps tell our brand story and convey...

More Insights From This author