Is Your Retirement Plan Really Future-Proof? Critical Questions Every Business Owner Should Ask

Bottom Line Up Front

- Maximizing your contributions is key, with options like 401(k) plans, SIMPLE IRAs, and Cash Balance Plans providing tax advantages and flexibility.

- Flexibility and scalability are vital as your business grows, ensuring your retirement plan can adapt to workforce expansion and changing regulations.

- Regular reviews of your plan, compliance with legislation, and economic preparedness are necessary steps to secure a resilient and sustainable retirement plan for the future.

In today’s rapidly changing economic landscape, having a well-structured retirement plan isn’t just a perk for your employees – it’s a strategic investment in your company’s future. Small business owners, in particular, face unique challenges when offering retirement benefits, from maximizing tax advantages to navigating legislative changes. With evolving market conditions, new employee expectations, and shifting regulations, it’s never been more critical to ensure that your retirement is built to last.

Future-proofing your retirement plan means asking the tough questions now to avoid costly mistakes later. Is your plan flexible enough to grow with your business? Are you taking full advantage of tax incentives? Are you prepared for legislative changes that could impact compliance?

In this guide, we’ll review the key questions every business owner should consider to ensure your plan stands the test of time. Whether you’re already offering a plan or just starting, these insights will help secure both your business’s and your employees’ financial future.

Are You Maximizing Contribution Opportunities?

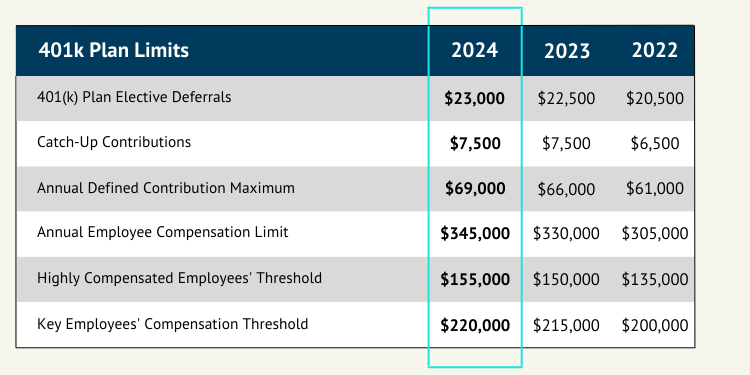

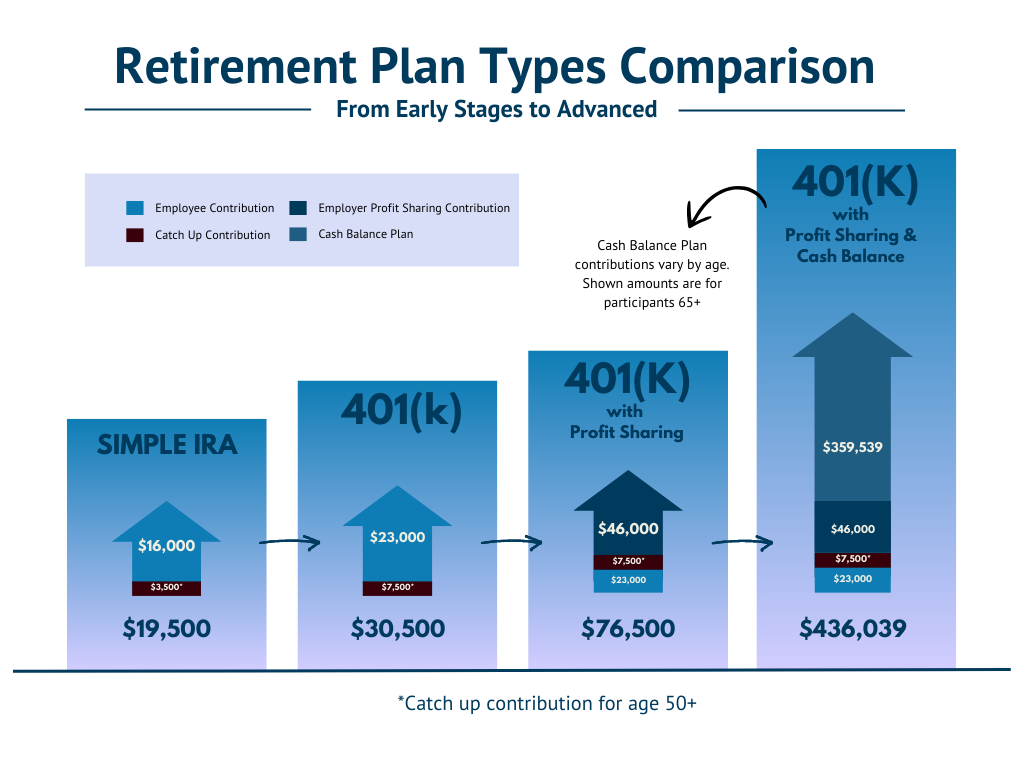

Each year, the IRS sets contribution limits for retirement plans like 401(k)s and profit-sharing plans. Are you contributing the maximum allowable amount? Missing these limits could mean leaving valuable tax-deferred growth on the table.

Business owners can often contribute more than employees through profit-sharing components or catch-up contributions if they’re 50 years or older, making this a prime area for tax savings and retirement growth.

- 401(k) Limits: The contribution limit in 2024 is $23,000, with an additional catch-up contribution of $7,500 for those aged 50 years and above (higher catch-up contributions are coming in 2025 for those aged 60-63).

- SIMPLE IRA Limits: Employees can defer up to $16,000 of their salary pre-tax, with a $3,500 catch-up contribution for those aged 50 years and above.

2024 Cash Balance Plan Contribution Limits

Does Your Plan Offer Flexibility for Growth?

As your business grows, your retirement plan needs to grow with it. A common mistake is setting up a plan that works well for your current size but doesn’t leave room for expansion. Your retirement plan should be flexible enough to grow with your business and adapt to changes in your workforce, revenue, and long-term goals.

Ask yourself:

- Can your plan scale with your business? Whether you plan to double your workforce or add employees gradually, your plan should allow for increased contributions as profits rise or provide options to enhance benefits without straining cash flow.

- Is your plan portable and adaptable? Employees are more likely than ever to change jobs. Offering portability (e.g., easy rollovers) and flexible vesting schedules makes your plan more attractive while supporting long-term employee retention.

Are You Prepared for Legislative Changes?

Retirement plan regulations are always evolving. Recent updates, such as the SECURE Act and SECURE 2.0, have reshaped the retirement landscape with changes like higher contribution limits and expanded eligibility for part-time employees. Keeping your plan compliant is crucial to avoiding penalties and missing out on tax benefits.

Key steps to take:

- Regular plan reviews: Work with your administrator or actuary to ensure your plan aligns with the latest legislation, like changes to required minimum distributions (RMDs), or auto-enrollment provisions.

- Maximizing tax incentives: Under SECURE 2.0., small businesses starting new plans may qualify for increased tax credits, and features like automatic enrollment or matching or matching contributions can unlock additional savings.

Have You Accounted for Economic Uncertainty?

No one can predict the future, but a resilient retirement plan should be prepared to handle market fluctuations, recessions, inflation, and other economic challenges.

Is Your Investment Strategy Diversified?

A well-diversified investment strategy is key to weathering economic storms. Offering a mix of conservative and growth-oriented options like equity, bonds, and stable value funds helps manage risk. Diversification is also crucial for businesses – evaluating the plan’s risk exposure and using flexible matching formulas can maintain financial stability without overextending resources.

Can Your Plan Handle Economic Shocks?

Retirement plans must be built to withstand economic shifts. According to data from the Center for Retirement Research at Boston College, the average retirement age for men is 65, and for women, it’s 63. Assuming most people start saving at around age 25, that’s at least 35 years of managing retirement savings before tapping into them.

Think about the last 35 years: we’ve seen significant economic events, the most recent being the COVID-19 pandemic. This disruption underscored the importance of flexibility, as many companies had to adjust or pause distributions. Ensuring your plan includes loan or withdrawal options for employees facing financial hardship can offer them a safety net without compromising their long-term savings goals.

Do You Have the Right Team?

An experienced team of professionals – actuaries, recordkeepers, plan administrators, and financial advisors – is essential for designing and maintaining a successful retirement plan. They help ensure compliance, manage risk, and optimize contributions.

Key Roles:

Actuary: Modesl scenarios based on business growth and market conditions to keep the plan sustainable.

Recordkeeper: They provide the investment vehicles, track daily balances for each participant, and facilitate distributions.

Financial Advisor: Helps select investment options that align with employee goals and risk tolerance.

Plan Administrator: Whether in-house or a third-party administrator, they ensure the day-to-day operations run smoothly, from timely contributions to monitoring compliance and addressing regulatory changes.

Are You Conducting Regular Plan Reviews?

Regular annual or semi-annual reviews can ensure your plan remains compliant, competitive, and aligned with your long-term goals. These reviews should cover:

- Plan participation and employee engagement

- Investment performance and risk management

- Compliance with the latest legislation

- A cost-benefit analysis of employer contributions

By conducting regular reviews, you can spot areas for improvement and ensure your plan continues to meet both your financial and operational objections.

Future-Proofing Starts Now

A well-structured retirement plan can be one of the most valuable assets you offer your employees, helping attract and retain top talent. Future-proofing is an ongoing process that requires flexibility, expert guidance, and regular reviews. At Odyssey Advisors, we specialize in designing and administering customized retirement plans tailored to your company’s goals. Whether you’re starting a new plan or refining an existing one, we’re committed to being your partner for the long haul.

Ready to future-proof your retirement plan? Contact Odyssey Advisors today to schedule a consultation.

Disclaimer: None of the above information should be construed as financial, investment, or legal advice. Please consult your financial advisor or ERISA attorney to address your specific needs.

About The Author Stephanie joined the Odyssey Advisor’s team all the way from the Lonestar state in November of 2020. She is versatile in her abilities and has experience in copywriting, photography, and analytics. She helps tell our brand story and convey...

More Insights From This author